CO2 Accounting

What are Scope 1, 2, and 3 CO2 emissions?

.avif)

%20(1).avif)

What are Scope 1, 2 and 3 CO2 emissions?

We address all your important questions regarding emissions here:

- What are Scope 1, 2 and 3 emissions? What are direct and indirect emissions?

- (Direct) Scope 1 Emissions

- (Indirect) Scope 2 Emissions

- (Indirect) Scope 3 Emissions

What are Scope 1, 2 and 3 emissions? What are direct and indirect emissions?

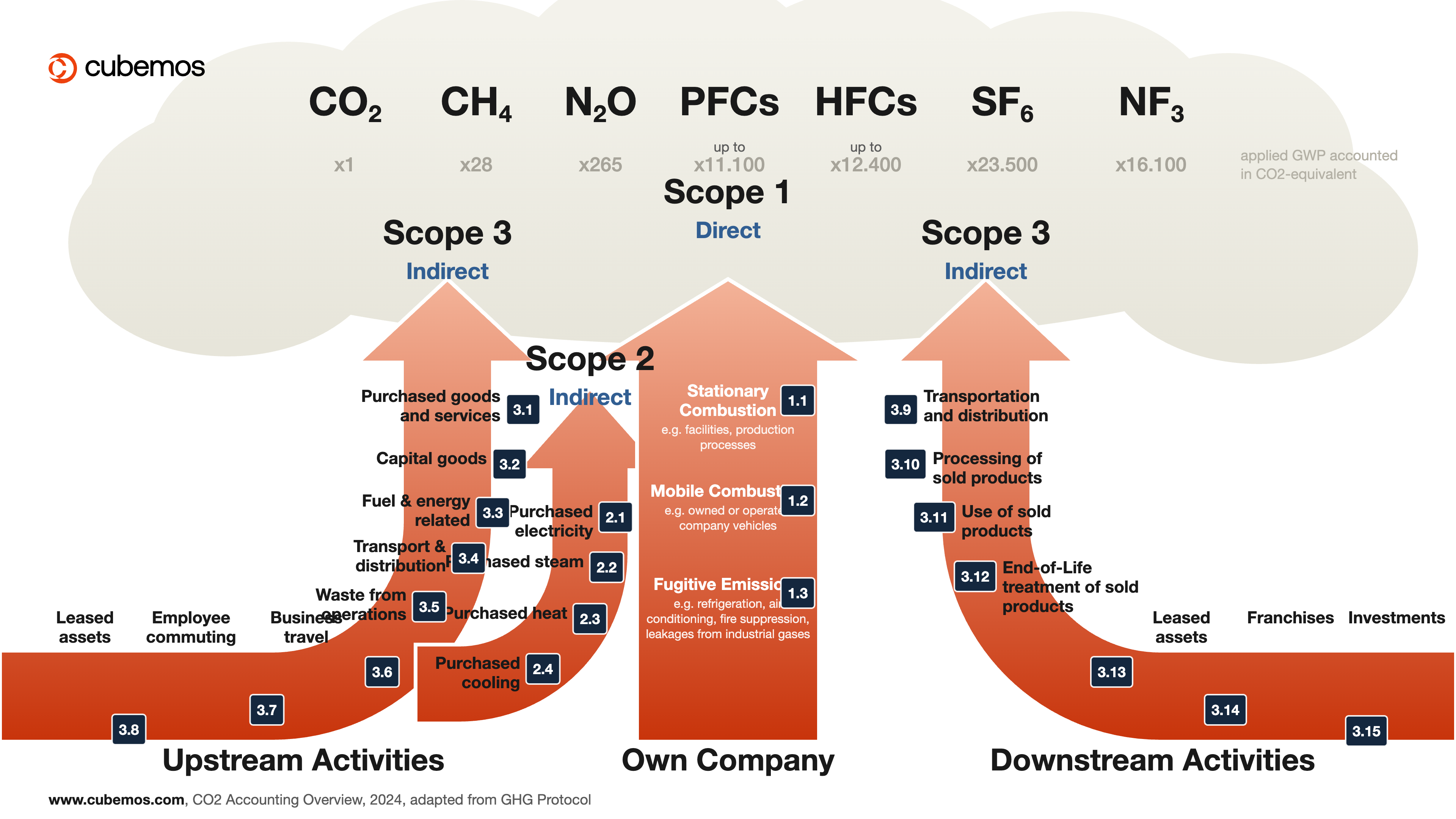

The GHG Protocol Corporate Standard defines three types of greenhouse gas emissions, as shown in the following infographic:

- Scope 1 (direct emissions): The emission sources are owned or controlled by the reporting company.

- Scope 2 and Scope 3 (indirect emissions): The emission sources are owned or controlled by another company, but result from the activities of the reporting company. Scope 2 is purchased energy, while Scope 3 includes all other indirect emissions.

Companies using the GHG Protocol are required to report on Scope 1 and 2 emissions. Reporting on Scope 3 is voluntary but recommended, especially since Scope 3 can account for more than 90% of a company's emissions. For example, Scope 3 accounts for almost 100% of Apple's emissions.

Scope 1 Emissions

Scope 1 emissions are direct emissions from sources owned or controlled by the reporting company. Examples include fossil fuels burned on-site or in the company's vehicle fleet. Scope 1 emissions are divided into four categories:

- Stationary: Emissions from the combustion of fuels in a facility for generating electricity, heat, or steam (e.g., boilers, turbines, furnaces, incinerators, etc.). All fuels that generate greenhouse gas emissions must be included in Scope 1.

- Industrial Processes: Emissions released during the production or processing of materials or chemicals such as cement, aluminum, ammonia, waste treatment, etc.

- Mobile: Emissions from the combustion of fuels in company-owned or controlled mobile sources (e.g., trucks, ships, cars, aircraft, mobile machinery, etc.). Note that electric vehicles may fall under Scope 2 emissions.

- Fugitive: Intended or unintended release of greenhouse gases during the operational lifetime of facilities (e.g., hydrofluorocarbon emissions from refrigeration and air conditioning systems, leaks from joints/seals, methane emissions from coal mines and venting, fire suppression systems, methane leaks from natural gas transport, etc.)

The GHG Protocol offers calculation tools and online training for companies to calculate emissions using the Corporate Standard.

Scope 2 Emissions

Scope 2 emissions are indirect emissions resulting from the consumption of purchased energy such as electricity, heating, or cooling. This also includes energy purchased for company operations or the operation of its own vehicle fleet. Scope 2 is indirect because the emissions arise from the reporting company's energy consumption but are released outside its controlled facilities. Accounting for Scope 2 emissions is important because almost 40% of global greenhouse gas emissions are attributable to energy generation, and half of this energy is consumed by companies. Purchased energy also typically offers companies the greatest opportunities for savings. Examples include implementing energy efficiency measures, participating in green electricity markets, or installing on-site combined heat and power plants.

There are two methods for calculating Scope 2: a market-based or a location-based approach. They represent different ways to "attribute" the GHG emissions from energy generation to end-users of a specific grid. The market-based approach reflects the emissions from a specific electricity supplier or a single electricity product chosen by the reporting company. The location-based approach reflects the average emissions intensity of the grids where electricity consumption occurs.

The GHG Protocol offers comprehensive guidance and online training for companies to calculate Scope 2 emissions using both approaches.

Scope 3 Emissions

Scope 3 emissions are the remaining indirect emissions that result from a company's activities not related to purchased energy. Examples include the production of purchased materials, business travel, product distribution, and end-of-life treatment. There are 15 categories of Scope 3 emissions, divided into upstream and downstream activities:

Scope 3 Categories: Upstream Activities No. 1-8

These are indirect GHG emissions associated with purchased or acquired goods and services that occur up to the point of receipt by the reporting company.

Scope 3 Categories: Downstream Activities No. 9-15

These are indirect GHG emissions associated with sold goods and services that occur after they have been sold by the reporting company and/or control has been transferred from the reporting company to another entity.

Overview of Scope 3 Categories

- Purchased goods and services include the upstream emissions of purchased goods and services. This includes the extraction, production, and transportation of goods and services acquired by the reporting company in the reporting year that are not included in other upstream categories.

- Capital goods, sometimes referred to as capital assets, are long-lived end products used by the company to manufacture or provide a product or service. Examples include plant, machinery, buildings, facilities, and vehicles. This category includes all upstream emissions resulting from the extraction, production, and transportation of capital goods acquired by the reporting company in the reporting year. Note that emissions from the use of capital goods are accounted for in either Scope 1 (for fuel consumption) or Scope 2 (for electricity consumption).

- Fuel- and energy-related activities not included in Scope 1 or 2. This includes the upstream emissions from purchased fuels and electricity by the reporting company. Examples include coal mining, fuel refining, natural gas extraction/distribution, etc.

- Upstream transportation and distribution of products purchased by the reporting company from upstream suppliers in the reporting year. This includes emissions from the transportation of purchased products by air, rail, road, and ship, as well as from third-party transportation and distribution services and the storage of purchased products.

- Waste generated in operations includes emissions from the disposal and treatment of waste from the reporting company's own or controlled operations in the reporting year by third parties. Examples include landfill disposal, wastewater, incineration, composting, etc.

- Business travel includes emissions from employees traveling for business purposes in vehicles owned or operated by third parties. Examples include air travel, rail travel, bus travel, rental cars, etc.

- Employee commuting includes emissions from employees commuting between their homes and workplaces. Examples include travel by car, bus, train, plane, subway, etc. Companies may also include emissions from employees traveling for telework in this category.

- Upstream leased assets include emissions from operational assets leased by the reporting company in the reporting year that are not already included in Scope 1 or 2 inventories. In this case, the reporting company is the lessee.

- Downstream transportation and distribution of products sold in vehicles and facilities not owned or controlled by the reporting company in the reporting year. This includes downstream emissions from the transportation of sold products by air, rail, road, and ship, as well as from third-party transportation and distribution services and the storage of sold products.

- Processing of sold products refers to emissions that occur during the processing of intermediate products in the reporting year. Intermediate products are precursors to final products or services that require further processing before they can be used by the end consumer. An example would be an engine included in a car. The reporting company's Scope 3 emissions here include the Scope 1 and 2 emissions of downstream value chain partners, such as the car manufacturer.

- Use of sold products includes emissions from the use of goods and services sold by the reporting company in the reporting year. The reporting company's Scope 3 emissions here include the Scope 1 and 2 emissions of end-users. There are two types of use-phase emissions – direct and indirect. Direct use-phase emissions include products that directly consume energy (e.g., cars, data centers) and fuels (e.g., natural gas, coal), as well as products that contain or release greenhouse gases during use (e.g., refrigeration units, fertilizers). Indirect use-phase emissions include products that indirectly consume energy during use (e.g., clothing that needs to be washed and dried, food that needs to be refrigerated). Reporting companies must report direct use-phase emissions, while indirect use-phase emissions are optional.

- End-of-life treatment of sold products includes the total expected emissions from waste disposal and end-of-life treatment of products sold by the reporting company in the reporting year. Examples include landfilling, incineration, recycling, etc. If the sold product is an intermediate product, the reporting company should account for emissions from the end-of-life of the intermediate product, not the final product.

- Downstream leased assets include emissions from operating assets owned by the reporting company and leased to other entities in the reporting year that are not already included in Scope 1 or 2 inventories. In this case, the reporting company is the lessor.

- Franchises include emissions from the operation of franchises that are not included in Scope 1 or 2 for the reporting company.

- Investments include emissions associated with the reporting company's investments that are not included in Scope 1 or 2 for the reporting company. This category mostly applies to investors, banks, and other financial institutions.

The GHG Protocol provides comprehensive guidance and online training for companies on calculating Scope 3 emissions.

.avif)